Residents stand on a street waiting for nucleic acid test during lockdown amid the coronavirus disease (COVID-19) pandemic, in Shanghai, China, April 17, 2022. (Aly Song/ REUTERS/ TPG images)

Irregular Unemployment and China’s ‘Last Generation’

2022 put an end to a core belief many Chinese people had harbored: as long as one works hard enough, life will keep improving.

Quick Takes

- China’s irregular unemployment over the last two years was a result from top-down policies rather than a natural consequence of economic restructuring or social changes.

- China’s internet sectors and private Micro-, Small and Medium-sized Enterprises are crucial for youth employment. However, several political actions have left these sectors battered, and the young generation lost confidence in their job prospects.

- Many young people refuse to marry, have children, or become ‘mortgage slaves”, despite the government’s U-turn towards boosting the economy (again). There is a ‘decoupling’ between the development the state wants and young people’s development visions.

2022 has taken its place as a sea change in the history of China. When the country joined the WTO in 2001, the Reform and Opening-Up era had moved into a frenetic globalization phase. Jiang Zemin, the former General Secretary of the CPC, who passed away at the end of 2022, had previously defined the first two decades of the 21st century as “a period of great strategic opportunities,” which the party must seize tightly to “develop the economy, improve democracy, advance science and education, enrich culture, foster social harmony and upgrade the texture of life for the people.”

However, by 2022 the world’s second-largest economy came to a standstill, and industries hemorrhaged. Lockdowns and quarantines proliferated. International travel ceased. Cities’ pandemic controls discriminated against each other’s residents. Unemployment became a reality for many more people, young people especially: the official unemployment rate for urban & township 16–24-year-olds nudged the 20% mark in 2022 (up from 9.6% at the start of 2018).

On the one hand, as a 2020 Echowall article sets out, slowing growth and flagging demand already meant China faced an immense challenge only to maintain employment levels. On the other hand, the unemployment wave of the past two years has been something else. Irregular unemployment has resulted from top-down policies rather than a natural consequence of economic restructuring or social changes.

With young people at the forefront, an extraordinary series of demonstrations broke out around the country in November 2022, followed by the sudden scrapping of China’s stringent pandemic control system in early December. The annual Central Economic Work Conference in mid-December put the “private sector front and center in fresh vows to stabilize and bolster [the] economy.” The leadership was “looking to bolster the digital economy while supporting platform companies in enhancing development, creating jobs, and competing in the global market.”

It would be funny if it were not sad. The internet economy, and indeed the private sector as a whole, have been dealt savage blows by several political actions over the last two years. Redundancies have been widespread. Will the latest U-turn manage to reinvigorate things? If the young generation loses confidence in their job prospects and future, the employment crisis will remain a medium-term headache for China. The following analysis will look at China’s internet sectors and private MSMEs (Micro-, Small and Medium-sized Enterprises), crucial vectors for youth employment, and set out the backdrop to China’s irregular unemployment and the immense socio-psychological toll this crisis has been having.

The Digital Economy and Young People’s Jobs

It was not just about having an outwardly-focused economy to shore up domestic growth; in the wake of WTO accession, the capital dividends from China’s globalization also fueled fast development for the internet sector. Vibrant venture capital markets helped the latter become pioneering, and the size of the national user population anointed the internet economy as one of the big engines of growth. More recently, consumption has been further stimulated by the way internet platforms have become deeply entwined with conventional economic sectors. Internet celebrities promoting merchandise, social media, online shops, the sharing economy, and big data analytics have integrated to turn shopping and everyday life into a stream of internet scenarios in a China-style economic ecosystem known as “internet+.”

Unlike what most Western analysts would have you think, “internet+” was not something willed into being by the Chinese state. Nevertheless, it, a brainchild of businesspeople, started as the title of a speech given in December 2012 by Yu Yang, founder of the internet consultancy Analysys International, where he argued that all traditions and services would end up being transformed by the internet and a new economic paradigm would emerge. The catchphrase “internet+” (互联网+) soon took on, particularly among Chinese internet giants such as Tencent. Premier Li Keqiang made his first announcement of an official “Internet Plus” action plan in his Government Work Report in 2015. The plan was to “encourage the healthy development of e-commerce, industrial networks, and Internet banking, and to guide Internet-based companies to increase their presence in the international market”.

This vibrant sector drew in countless young job seekers. 32.9% of China’s working population is under 35 (census figures from 2020), but that proportion rises to 70.4% among those working in the internet and related service businesses. 16.77 million people were working in the internet sector in 2018, with 65% based in major eastern cities (Beijing, Shanghai, Guangzhou, Shenzhen, Hangzhou). As an Echowall article in early 2020 clarifies, “in a relatively low-wage, low-welfare China where real estate prices have skyrocketed, the tech sector provided higher salaries, year-end bonuses, the prospect of advancement and higher social prestige.” Despite the intensity of the job and the amounts of overtime called for, working in the IT and internet sectors has consistently been a top aspiration for college graduates.

At the same time, not only highly-qualified staff but also ordinary working-class people have found employment thanks to the platform economy. Over 60% of the rural-based labor force has ended up in occupations to do with digital platforms, such as food delivery riders. They also make up a significant share of social media content creators, online shop owners, and streamers. Although there are even fewer labor rights safeguards for these kinds of “flexible” work, they appeal more to younger rural migrants than a monotonous life on assembly lines. There were a total of 6.23 million platform workers in these new forms of employment in 2019, and another 78 million jobs existed thanks to spin-off effects from the platforms.

Political Interference and the Hobbling of the Platform Economy

In a further boost to the internet industry, the onset of the coronavirus pandemic in 2020 shifted even more economic activity online. At the end of 2020, China boasted 197 digital platform companies with valuations over US$ 1 billion, double the number in 2015. They posted rapid 56.3% counter-cyclical value growth against a sluggish global economic backdrop.

Everything changed, though, with a series of policy strikes against the industry. A stunning reversal of the trend ensued.

When Alibaba founder Jack Ma spoke at the Shanghai Finance Forum in October 2020, he accused the financial regulators of “running an airport like it was a train station.” As a consequence, the impending US listing of his company Ant Financial (spun out of Alibaba) came to an abrupt halt, while Ma himself was summoned to appear before four central authorities acting in tandem. (In January 2023, the Ant group announced that Jack Ma is to cede control of the company)

Screenshots – video from Sina of Alibaba founder Jack Ma spoke at the Shanghai Finance Forum on October 24, 2020.

The Communist Party’s United Front Work Department issued an Opinion on Strengthening the United Front Work of the Private Economy in the New Era in September 2020: they called for “strengthened United Front and political & ideological work focusing on private enterprises.” Businesspeople must “maintain a high degree of uniformity with the Central Committee and always be politically aware people”.

This incident was seen as the first chain of dominoes, as the government resolved to act against private enterprises and their owners’ increasing influence. An ‘anti-monopoly wave’ swept over the internet industry. The Central Economic Work Conference called for “enhanced anti-monopoly work and prevention of the unchecked expansion of capital” at the end of 2020. The State Council Anti-Monopoly Commission followed up in February 2021 with its Anti-Monopoly Guidelines for the Platform Economy Sector. Alibaba was duly accused on 10 April of breaching the Anti-Monopoly Law and fined 18.2 billion yuan, the most significant antitrust penalty in Chinese history and one greater than the total of antitrust fines levied from 2008-2019.

An “administrative guidance session” on the treatment of internet platform companies was held in 2021. The order was laid down to “make full use of the deterrent effect of the Alibaba case; internet platform companies must be disciplined and watch their step.”

An “administrative guidance session” on the treatment of internet platform companies was held three days later by the State Administration for Market Regulation in conjunction with the Cyberspace Administration of China and the State Administration of Taxation. The order was laid down to “make full use of the deterrent effect of the Alibaba case; internet platform companies must be disciplined and watch their step.” A flurry of crackdowns followed various sectors of the platform economy. In October 2021, Meituan, the largest player in the meal delivery sector, was hit with a fine for monopolistic practices of 3% of annual sales, i.e., 3.442 billion yuan.

The private education and training sector was already running afoul of the government’s ideological bent and ended up being hit hard. In 2016, over 75% of K-12 (from kindergarten to 12th grade) students in China were taking after-school tutoring. In the last few years, private online tutoring services have been growing particularly well: 90% of the 116.4 billion yuan in financing for the private education industry in 2020 flowed into online education. The high salaries available attracted numerous young people to work in the internet sector. Official estimates are that up to ten million people nationwide have been engaged in education and tutoring provision, 90% under the age of 35 and 80% holding an undergraduate degree or above.

The State Administration for Market Regulation announced the maximum possible penalties for 15 tutoring providers on 1 June 2021, amounting to a total 36.5 million yuan in fines. The Ministry of Education decreed in July that tutoring companies serving K-12 students must register as non-profit entities, online academic providers would now have to obtain approval, and these would be prohibited from raising market funds or operating on a capitalized basis.

State supervision of young people’s lives outside the classroom extended into online gaming too, in this, the world’s largest online gaming market. In a 30 August 2021 decree, the National Radio and Television Administration ordered all online games providers not to provide service to users under 18 except for 1 hour from 8-9 pm from Fridays to Sundays and on public holidays.

‘Cyber information security’ was another cudgel wielded against China’s internet industry in 2021. The Cyberspace Administration published a draft for comments on its Cybersecurity Review Measures on 10 July, providing that “where operators holding personal data of over 1 million users list abroad, they must apply for a review at the Cybersecurity Review Office”. The first company to fall afoul of this regulation was the ride-hailing provider Didi Chuxing, freshly listed in New York on 30 June 2021. On 2 July, the CAC announced it was under a cybersecurity review. On 4 July, new Didi user registrations were suspended in China, also ordering its app removed from Chinese app stores. Didi announced a “voluntary” delisting from the New York Stock Exchange in May 2022, its share price has fallen nearly 90% from the IPO level, and its valuation has shrunk by over US$ 60 billion.

Waves of layoffs in the internet industry

Like Didi, almost all Chinese internet companies saw their valuation plummet from spring 2021 to 2022. A graph went viral in the spring of 2022 under the title “Changes in market cap for Chinese tech and internet companies over two years.” Apple’s market capitalization in April 2020 had been roughly equal to the sum total of China’s Alibaba, Tencent, Meituan, JD.com, and Pinduoduo; by April 2022, however, Apple’s valuation had more than doubled, whereas the latter five Chinese companies were shadows of their prior selves. Even when the 44 next-biggest Chinese tech and internet stocks were added, the Chinese sector still lagged Apple in size by US$ 1.26 trillion.

By October 2022, Tencent’s share price had declined by around 70% from its February 2021 peak, with around HK$ 5 trillion market value disappearing into thin air. For its part, Alibaba’s Hong Kong share price dropped 77% over two years, burning through another HK$ 5 trillion in market capitalization.

The carnage of the sector’s last two or so years has translated into frequent layoffs and staff cuts. 49.9% of respondents interviewed for the Internet Industry Staff Movements Research Report 2021 said the internet company they worked at had laid off staff, and 25.1% included themselves during the year. Reported figures point to over 35 well-known internet companies laying off staff in 2021, with, for example, 12% headcount reductions at iQIYI, 30% at the short video platform Kuaishou, and more or less complete wipeouts at K-12 education and tutoring providers. New Oriental (XDF) wound down its online after-school tutoring business in mainland China in October 2021, causing a 90% drop in its share value, an 80% drop in its business revenue, and 60,000 staff leaving their positions.

The waves of job losses continued to cause lasting pain to Chinese tech workers in 2022. Companies have been evasive on their precise layoff numbers, and online rumors have been difficult to substantiate. Nonetheless, social media was ablaze in March with the story of tens of thousands of layoffs at each of Alibaba and Tencent; the online discussion on Weibo received hundreds of millions of hits. Alibaba filings state that its staff headcount at the end of the third quarter of 2022 was 15,413, lower than at the end of 2021. The internet is a sunrise industry, and its leading players should normally stay on that trend regarding their staffing levels. If the latter remains level or goes down, that typically means large-scale structural layoffs; in China, the usual practice is to replace better-paid low-to-middle-rank staff with cheaper newcomers. Besides the industry giants, there are also concerns about widespread bankruptcies among small internet companies.

China’s "village swots” have to study much harder than their big-city peers to enter elite universities. For them, an IT degree represents a chance to change their destinies and secure an urban future, given the aphorism that ‘it is only programmers who can get by on real study alone instead of connections and resources.’

Since the wave of layoffs began in 2021, major cities have frequently been under coronavirus lockdown; all industries have had to rein in their business activities, and jobs have become even harder to find. Many young people from the countryside or small towns have elected to return home for a while due to the scarcity of jobs, the constant threat of urban lockdowns or quarantines, and stubbornly high rents. The former is known locally as “village swots.(小镇做题家)” Given the vast educational disparities, they had to study much harder than their big-city peers. They could only gain entry to elite universities by ceaselessly doing mock gaokao (college entrance exam) papers. For these people, an IT degree represents a chance to change their destinies and secure an urban future, given the aphorism that ‘it is only programmers who can get by on real study alone instead of connections and resources,’ and high salaries are on offer for them to boot. For the past two years, the internet sector’s vagaries have hindered many of their dreams of social mobility.

“Capillaries” of the Chinese economy

Compared to the tech giants, China’s private MSMEs get almost no attention from international media. Chinese economists, however, see them as the capillaries pumping blood through the economy, given the outsize role they play in raising labor productivity, creating jobs, reducing income disparities, and fostering competition. (In the tertiary sector, a medium-sized enterprise is one with 100-300 staff, a small one with 10-100 staff, and a micro-enterprise is fewer than ten people). 99% of China’s 48.42 million enterprises were SMEs at the end of 2021, figures from the Ministry of Industry and Information Technology indicate. Four hundred million individuals were employed in private and individual businesses in 2021. Private companies, especially small, medium, and micro-businesses, are the most significant segment in China’s foreign trade, contributing more than 58.2% of trade growth in 2021. The health of MSMEs is closely linked to regional growth; where the former are vibrant, the local economy and job market are, too.

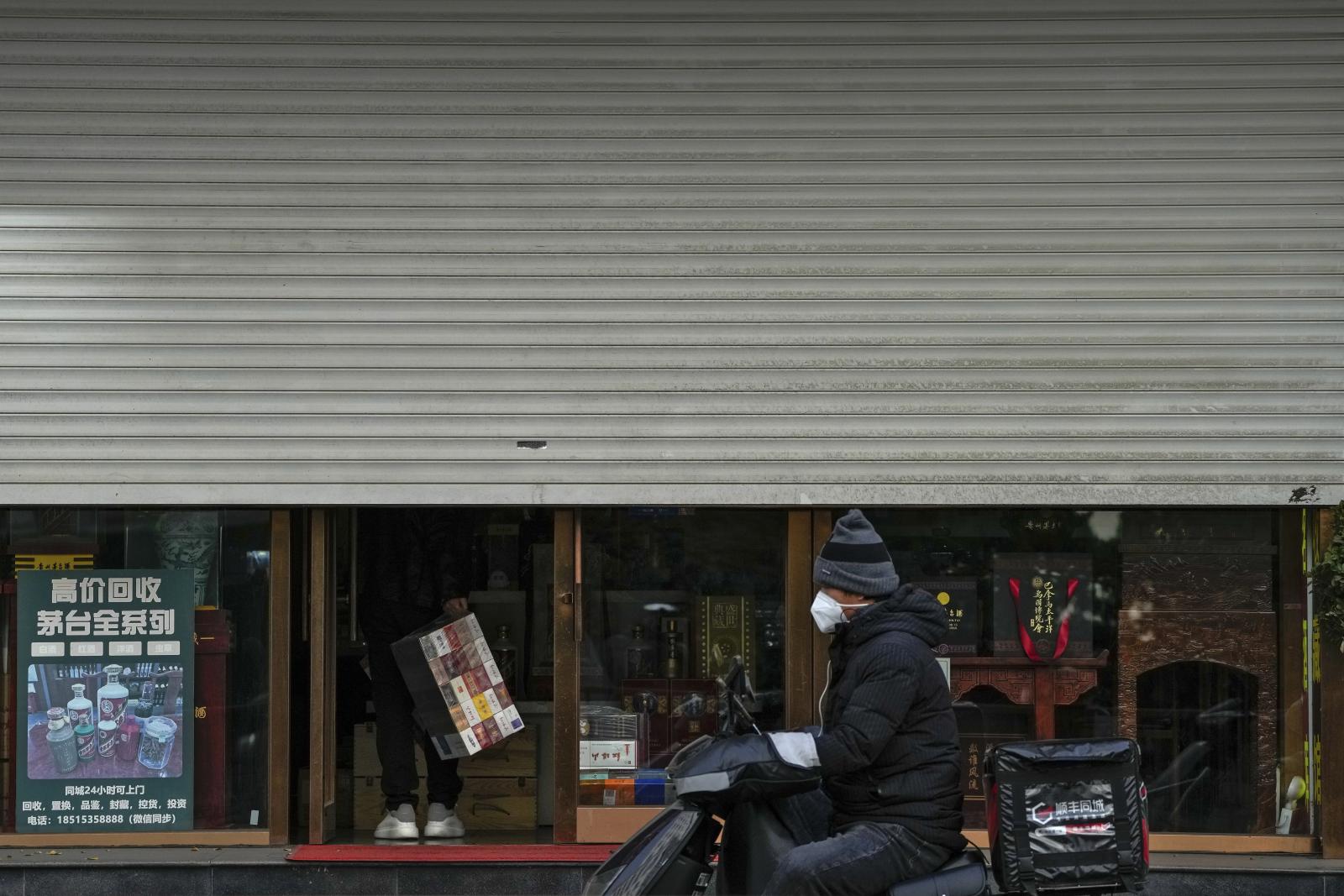

A delivery rider passes by a man carrying stack of cigarettes into his closure liquor store as part of COVID-19 controls in Beijing, Tuesday, Nov. 22, 2022. Anti-virus controls that are confining millions of Chinese families to their homes and shut shops and offices are spurring fears already weak global business and trade might suffer. (Andy Wong/AP Photo/TPG images))

The vibrant private economy provided a raft of employment and entrepreneurship options, from street restaurants to small supermarkets, not forgetting new consumer-related sectors such as website operation, online retail, yoga, and fitness classes. The market culture that gradually established itself during the Reform and Opening-Up era owes its greatest debt to private enterprises and individual businesses. However, when a major crisis suddenly swept the world, “smaller firms, informal businesses, and enterprises with limited access to formal credit were hit more severely by income losses stemming from the pandemic.”

Zero covid and the clogged capillaries

Shanghai was placed under “citywide static management and whole-population PCR screening” measures from the end of March to early June 2022. Many people were sealed off in their apartment buildings with daily necessities in short supply, some even going hungry or resorting to bartering for food. Shanghai’s daily consumption level dropped 80% from early March to early April. Chinese financial magazine Caixin estimates a 12.5% or roughly 225 billion yuan drop in Shanghai’s private consumer goods retail volume, a 9% or circa 103 billion yuan drop in manufacturing value-added, and potentially bigger losses (up to 328 billion) in associated cities.

A worker in protective gear prepares to deliver food in a cart with the words "Food delivery for the elderly" in the locked down Jingan district in western Shanghai, China, Friday, April 1, 2022. (Chen Si/AP Photo/ TPG images)

.jpg){kind=link}